Demystifying GSTR-9 — Part 1: GST Annual Return Form & Eligibility

Note: The due date to file annual GST return form GSTR-9 for FY 2018-18 has been further extended to November 30, 2019.

Businesses throughout India have experienced dissatisfaction filing returns under the Goods and Services Tax (GST), the biggest tax reform ever. The GST Council originally designed GST return forms so that all transactions would be in sync with each other, and so that no transaction between buyers and sellers would be left unrecorded. In the process of bringing these goals to fruition, return filing has become cumbersome. In response, the GST Council has made multiple attempts to simplify return filing for taxpayers.

Here’s a series of two articles attempting to shed light on the GSTR-9 annual return.

This first article, Part 1, will cover the basics of GSTR-9, types of forms and their formats, as well as eligibility.

The second article, Part 2, will cover issues related to filing, payment, and penalties.

What is GSTR-9?

GSTR-9 is the annual return that all registered, taxable people must file. Businesses are required to file this return annually by 31st December of the coming financial year (FY). In a recent announcement, CBIC extended due dates for filing GSTR-9, GSTR-9A, and GSTR-9C up to 31st August 2019.

The GSTR-9 return is a summary of a business’s monthly or quarterly returns, i.e., the total number of transactions in a particular financial year. It includes the amount of taxes paid (CGST, SGST, IGST) during the year, as well as details of exports or imports. In the December meeting, the GST Council also clarified that outward or inward supplies should be declared in annual returns as “supplies made during the financial year” and not “supplies as declared in GST returns filed.”

In simple terms, the purpose of the GSTR-9 is to consolidate information previously furnished in the monthly or quarterly returns. This implies that all monthly and quarterly returns must be filed before filing the annual return. Moreover, the GSTR-9 is not a rectification return but a consolidation return, which requires that data provided in monthly and quarterly returns must match the data on the GSTR-9 exactly.

Types of forms

Filing the GSTR-9 return involves the following forms:

GSTR-9A: This form is to be filed by taxpayers registered under GST’s composition scheme. It is a summary of all quarterly returns previously filed by the composition taxpayer. (Proviso to Sub Rule (1) of Rule 80)

GSTR-9B: This form is to be filed by ecommerce operators who have filed GSTR-8 during the previous financial year. It is basically an audited, annual account, duly certified by competent authority. (Sub Rule 2 of Rule 80)

GSTR-9C: This is a reconciliation statement to be filed by taxpayers whose annual turnover exceeds INR 2 crores (for all states) during the financial year. All such taxpayers are required to have their accounts audited by a Chartered Accountant, or Cost Accountant, and file a copy of their audited annual accounts. They must also file a reconciliation statement of tax already paid and details of tax payable as per audited accounts, along with this return.

Eligibility

All registered, taxable persons, except those listed below, are responsible for filing a GSTR-9 return, regardless of whether there were business operations during the year (i.e., even if all the returns during the period were NIL, a Nil Annual Return must be filed). This annual return is also required in cases where a taxpayer has cancelled their registration during the year.

However, the following persons are not required to file GSTR-9 as per Section 44(1) of the CGST Act, 2017:

- Input service distributors

- Non-resident taxable persons

- Casual taxable persons

- Persons paying tax under section 51 or 52 (i.e., persons paying TDS).

Furthermore, taxpayers opting for a composition scheme will file GSTR-9A in lieu of GSTR-9.

A registered person who has switched from regular to composition, or composition to regular, is required to file both GSTR-9 & GSTR-9A for the relevant period.

Broad overview of GSTR-9

GSTR-9 is divided into 6 parts and 19 tables

Part I: This part asks for basic details, such as the financial year, GSTIN, legal and trade names. These details will be auto-populated in the form.

Part II: This part asks taxpayers to provide details of outward and inward supplies declared during Financial Year (FY).

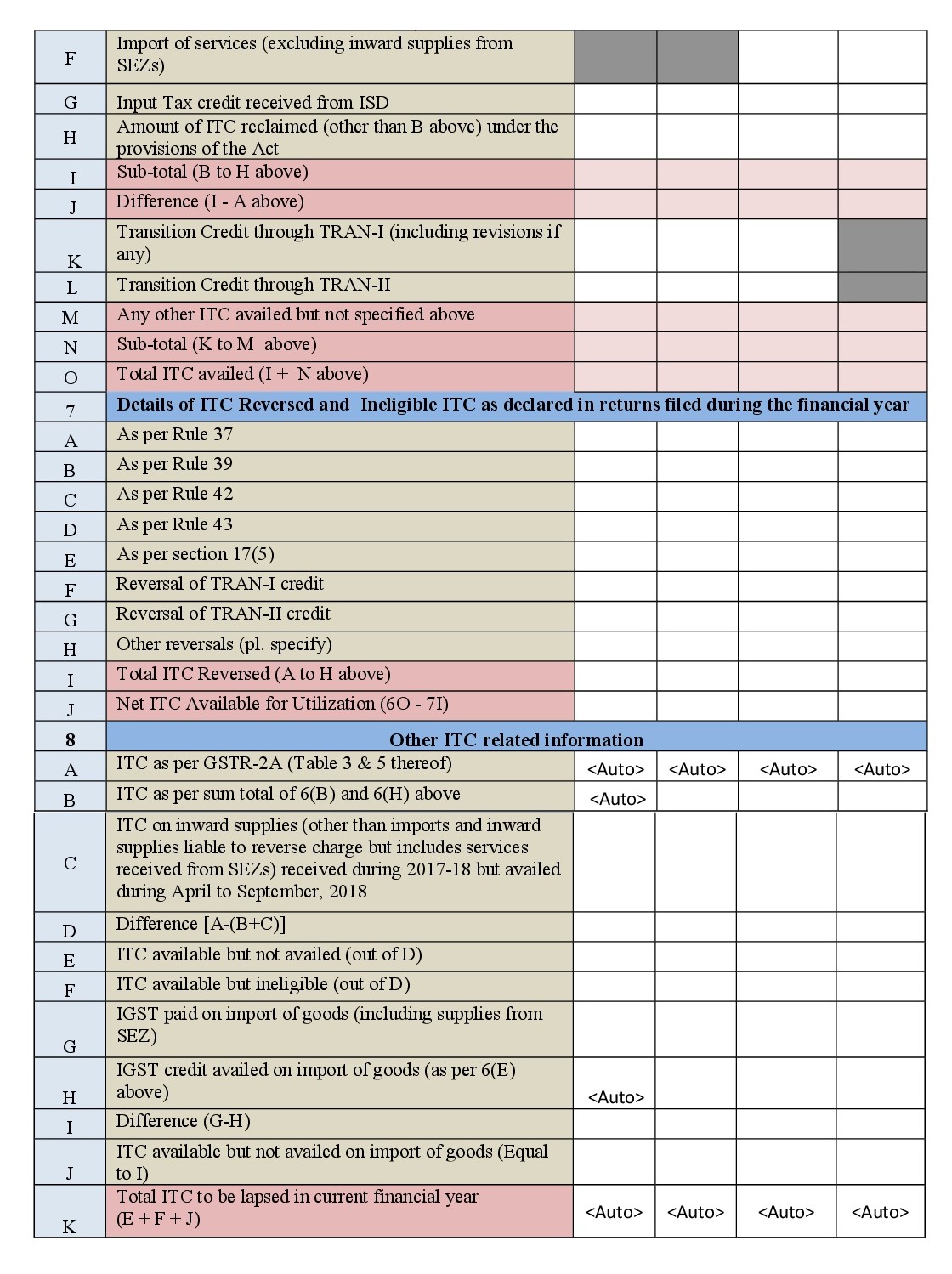

Part III: This is where taxpayers will provide details of the Input Tax Credit (ITC) as declared in returns filed during the financial year. Part III also asks for details of the ITC reversed and ineligible ITC as declared in individual returns.

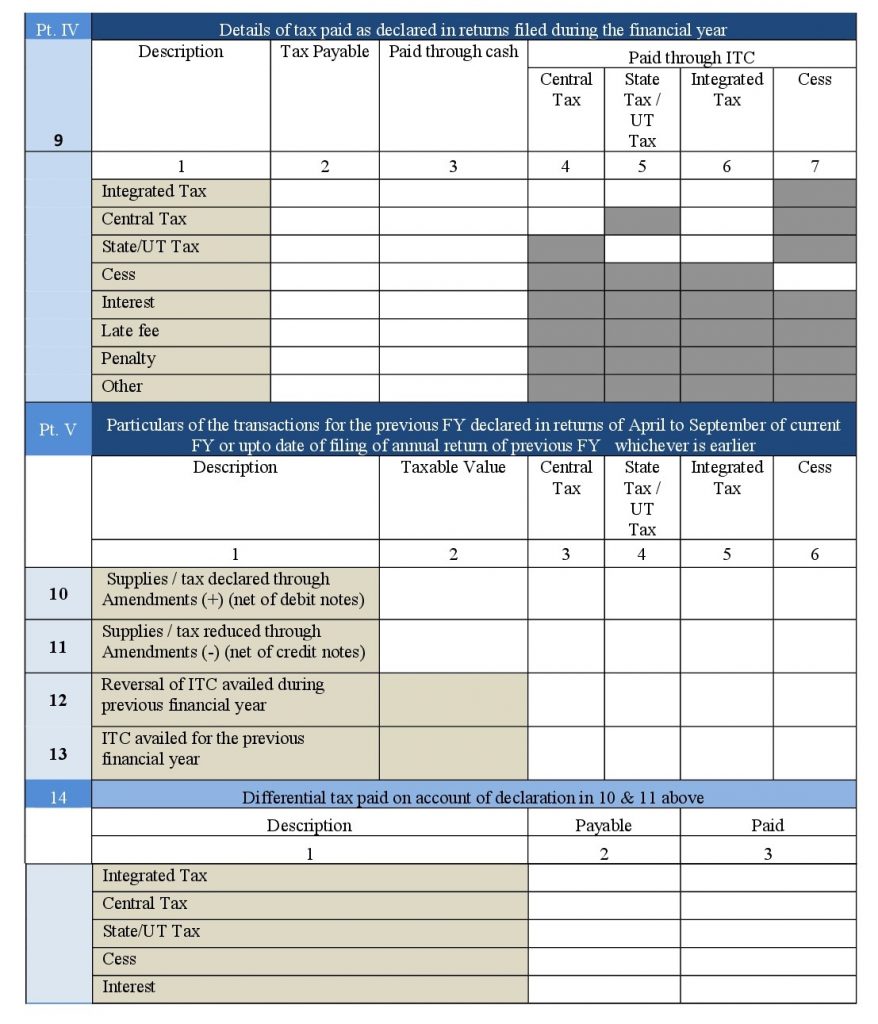

Part IV: Here, taxpayers will input details of taxes paid as declared in returns filed previously during the fiscal year.

Part V: This part asks for transaction particulars of the previous fiscal year, declared in returns from April to September of the current fiscal year, or up to the date annual returns of previous fiscal year were filed, whichever is earlier. Additional or omitted entries belonging to the previous fiscal year, but reported in current fiscal year, would be declared here as well.

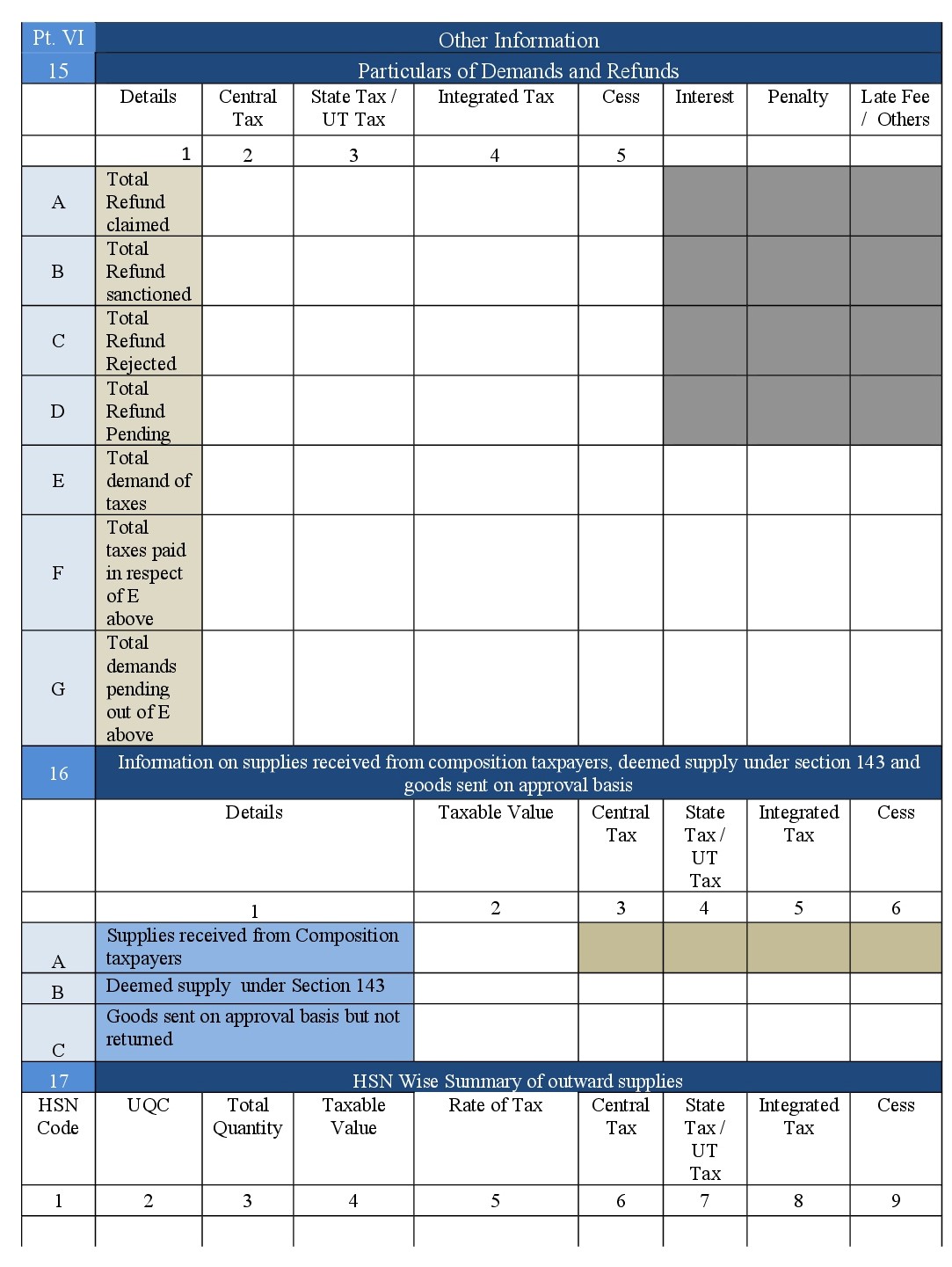

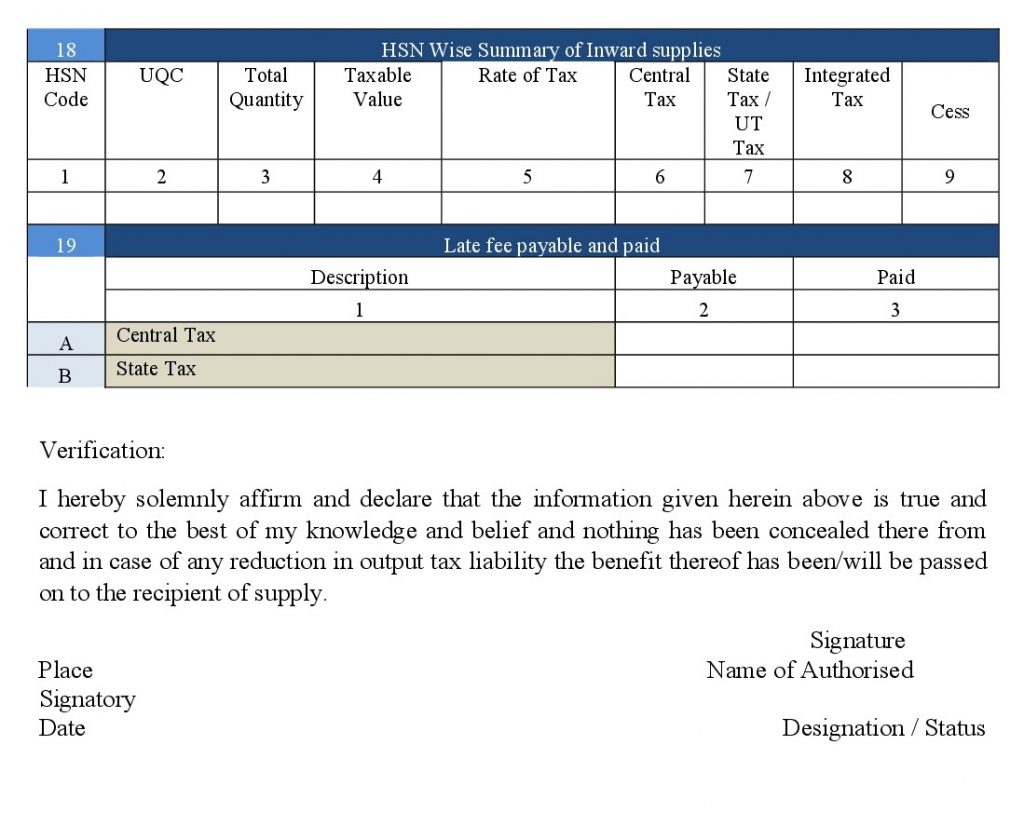

Part VI: Taxpayers will report other information here. This could include demand and refund details; supplies received from composition tax payers, deemed supply goods sent on approval basis; HSN-wise summary of outward and inward supplies; or late fees payable as well as those paid.

GSTR-9 Format

Prepare your business for e-invoicing under GST

Discover how to meet all compliance requirements while integrating e-invoicing into your tax function.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.