The Journey Towards GST 2.0 In A Nutshell

The new GST return or GST 2.0 was planned to be implemented earlier by October 2019 and has been deferred till April 2020. Here’s what you need to know about the new GST filing mechanism – the journey of GST return filing from the planning stage before the implementation of GST and right up to GST 2.0, a new GST filing mechanism.

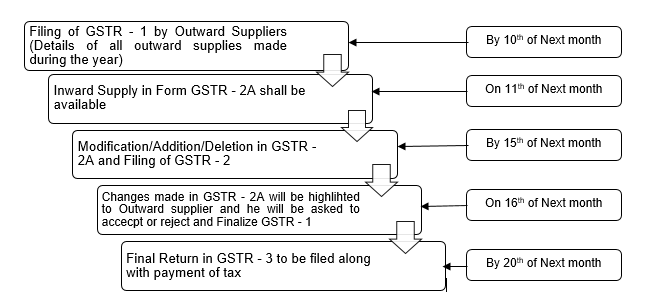

Planning of GST Return

Much before the introduction of GST law, there was a clear indication that the GST law will be a documentation driven law and matching of invoices will be of utmost importance. Accordingly, the filing of GST returns was made in phases. The below pictorial diagram shall provide ease of understanding of the same:

This entire process was found out to be too cumbersome and within the first month of filing, it was realized that filing of GST return is not an easy task. Also, the GST portal could not handle the pressure of filing such complicated GST returns. To rationalize, a stop-gap arrangement was made in filing Form GSTR – 3B.

Stop-gap arrangement

The Government rolled out a simplistic one-pager form in GSTR – 3B to self-declare the liability and Input Tax Credit available to the assessee and effectively disclose the net liability payable by the assessee. In the stop-gap arrangement, the filing of GSTR – 1 was continued, whereas filing of GSTR – 2 & GSTR – 3 was indefinitely deferred. To have better control over the liability of the assessee, the liability of GSTR – 3B and the sales invoices as reported in GSTR – 1 were matched online by the system and were being highlighted to assessees. The reports of GSTR – 2A were made available to the assessees only by end of 2018 but the filing of GSTR – 2 was still not made operational.

New Version of Returns 2.0

As highlighted earlier, the focus of GST law was to have documentation driven law with the matching of invoices to be of utmost importance to avoid any leakages of revenue. The proposed return structure has been framed in the following manner:

| Type of Assessee | Type of Return | Details to be submitted |

| Small Assessees (having turnover upto Rs. 5 crore) – Dealing with only B to C supplies | Quarterly return |

|

| Small Assessees (having turnover upto Rs. 5 crore) – Dealing with only B to B and B to C supplies | Quarterly return |

|

| Small Assessees (having turnover upto Rs. 5 crore) and having other transactions like Export, SEZ etc | Quarterly return |

|

| All the other Assessees | Monthly Return |

|

One may need to understand that the broad structure of returns can be understood as under:

- Each assessee needs to file Annexure 1 depending on the periodicity of filing return (this is similar to the filing of GSTR – 1 as being done presently). Interestingly the current Annexure 1 also requires filing of additional details as compared to GSTR – 1 for invoice level details of RCM liability

- Each assessee needs to file Annexure 2 depending on the periodicity of filing return (this is similar to proposed GSTR – 2 as being deferred presently). This particular form requires accepting or rejecting invoices as uploaded by their vendors in Annexure 1. Also, it has been provided that the Input Tax Credit can be taken by the assessee only to the extent of invoices reported in Annexure 1. In case invoices are not recorded, the maximum credit shall be to the extent of 20% of total credit reflected in Annexure 2

- Each assessee will be required to Main Return (this is similar to GSTR – 3 as being deferred presently).

It is believed that the new return structure is similar to the old mechanism as provided under the GST law.

Avalara is an experienced application service provider (ASP) and partner of authorized GST Suvidha Providers (GSPs). To understand how our cloud-based application Avalara India GST can help you with GST compliance automation, contact us through https://www.avalara.com/in/products/gst-returns-filing

For more information on GST and GST Compliance, visit www.avalara.com

Prepare your business for e-invoicing under GST

Discover how to meet all compliance requirements while integrating e-invoicing into your tax function.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.