What is a drop shipper and how does drop shipping affect sales tax?

Drop shipping can be a boon for online sellers, especially small businesses that don’t have the funds or space to keep inventory in stock. In drop shipping scenarios, a seller takes an order from a customer, then turns around and orders that item from a supplier, who ships it to the customer on behalf of the seller.

In many ways, drop shipping is a win for everyone involved. But because drop shipments involve one customer, two businesses, two sales transactions, and often two or three states, they tend to complicate sales tax compliance for both the seller and the supplier.

Do you have to collect sales tax in drop shipping transactions?

As with any sales tax situation, the first step toward determining whether you’re responsible for collecting and remitting sales tax is figuring out where you have nexus — a connection substantial enough to establish a tax obligation.

In general, if you have nexus with a state, you’re responsible for collecting and remitting applicable sales tax on sales to customers within that state. That’s true whether you use a drop shipper or deliver some other way.

How do you know if you have nexus with a state?

There are several ways to establish sales tax nexus with a state, but the two most common are through physical presence (physical nexus) or economic activity (economic nexus).

Physical nexus is created when you have real property in a state, like an office or brick-and-mortar store. Having employees in the state can also establish physical nexus — even if they’re only there temporarily — as can having inventory in the state (including inventory controlled by a marketplace facilitator).

Economic nexus is created when a business with no physical presence in a state meets or exceeds a state’s economic nexus threshold. Each state’s economic nexus threshold is unique. For example:

- California: $500,000 in total combined sales of tangible personal property delivered into the state by the retailer (and related entities), including nontaxable sales, in the current or previous calendar year

- Florida: $100,000 in taxable sales of tangible personal property in the current or previous calendar year

- Wyoming: $100,000 or 200 transactions of annual gross sales of tangible personal property, services, and admissions in the current or previous calendar year

Physical nexus was requisite until the Supreme Court of the United States overturned the physical presence rule in South Dakota v. Wayfair, Inc. (June 21, 2018), so economic nexus is a relatively recent phenomenon. See our state-by-state guide to economic nexus laws for state-specific information, or try our free sales tax risk assessment if you’re not sure whether you’ve established economic nexus with a state.

Drop shipping has always been tricky for sales tax precisely because both the seller and the supplier (aka, drop shipper) can have nexus and sales tax obligations — or not. And the tax complexity of drop shipping has only increased since Wayfair.

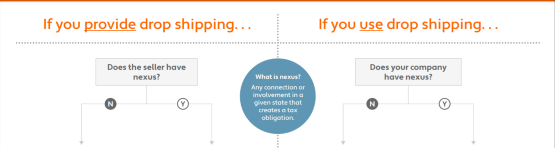

Sales tax obligations for a drop-shipping seller

If you’re the seller, you’re generally required to collect sales tax only if you have nexus with the customer’s state. As noted above, that typically occurs through physical presence or a certain threshold of economic activity in the state.

But that’s just one side of the transaction.

Sales tax obligations for a drop-shipping supplier

If you’re the supplier and you have nexus with the state where your customer (the seller) is located, you’ll need to do one of two things:

Charge your customer (the seller) sales tax, or

Collect a valid resale or exemption certificate from your customer (the seller).

As the supplier, you may also be required to collect and remit tax on a seller’s sales in states where you have nexus, but the seller does not. This is generally the case in California, Connecticut, Florida, Hawaii, and several other states.

Managing exemption certificates

A supplier’s sale to a seller is usually an exempt wholesale transaction because the seller is purchasing the goods to resell them. This is true even if the supplier has nexus and an obligation to collect sales tax in the seller’s state.

Nevertheless, if the goods sold are subject to sales tax in the state, the supplier must validate the exempt transaction by collecting a resale or exemption certificate from the seller. Without a valid resale exemption certificate, that transaction can be considered a retail sale rather than a wholesale sale, and the state could legally obligate the supplier to collect sales tax from its customer (the seller).

Resale exemption certificate procedures vary from state to state. Many states will accept an out-of-state resale certificate, multijurisdictional form (i.e., the Multistate Tax Commission uniform sales and use tax resale certificate or Streamlined Certificate of Exemption), or alternate documentation in a drop-shipping situation.

However, in California and other states that have stricter requirements for resale certificates, a seller must register with the state in order to obtain a valid exemption certificate from that state. Once registered, the seller would be obligated to collect sales taxes from customers in that state — even though the seller may not have any other nexus with the state.

Drop shipping rules prohibit a supplier from accepting a resale certificate from an unlicensed seller. And unless presented with a valid resale or exemption certificate, the drop shipper must charge sales tax to the seller, based either on what the supplier charges the seller or what the seller charges the consumer.

Bear in mind that state policies can change; Tennessee recently began accepting exemption certificates issued by other states where previously it did not.

The advent of economic nexus has increased the burden of exemption certificate management for many suppliers. According to Silvia Aguirre, vice president of Certificate Management at Avalara, suppliers that work with hundreds or thousands of sellers can end up having to collect and store hundreds, thousands, tens of thousands, or even hundreds of thousands of certificates — each of which could need to be produced in the event of an audit.

Simplify the complexity of drop shipping tax

Drop shipping can be a smart option for small sellers, but it can also add new layers of sales tax complexity. One way for small businesses to make the most out of drop shipping and other innovative solutions is to use Avalara sales tax automation software and exemption certificate management tools.

Have more questions about sales tax compliance? Check out our small business FAQ.

Updated February 24, 2022; originally written September 2, 2016.

Cover photo by Canva

Avalara Tax Changes 2026 is here

The 10th edition of our annual report engagingly breaks down key policies related to sales tax, tariffs, and VAT.

Stay up to date

Sign up for our free newsletter and stay up to date with the latest tax news.